Clarksons Research will soon release its full Chinese-language reports: Shipping Market Mid-Year Review 2025, Newbuilding Market Mid-Year Review 2025, and Shipping Industry Green Transition Mid-Year Review 2025.

Shipping Market

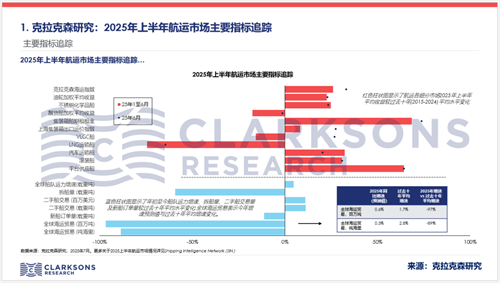

In the first half of 2025, the Clarksons Shipping Index saw a slight year-on-year decline of 5% to $24,101/day. However, excluding the containership market, the index dropped sharply by 31% year-on-year to $17,409/day, remaining 1% below the ten-year average.

During the same period, the Clarksons Containership Time Charter Index surged by 80% year-on-year and stood 80% above the ten-year average. The tanker market demonstrated resilience, with earnings largely stable compared to the second half of 2024 and 23% above the ten-year average, though down 33% year-on-year. Bulk carrier earnings fell 31% year-on-year but showed recent improvement, matching the ten-year average. Car carrier rates continued to adjust downward. LNG carrier earnings remained weak due to oversupply, while VLGC earnings retreated but recently rebounded to over $60,000/day.

Newbuilding and Secondhand Markets

Following a robust 2024 for newbuild orders and amid heightened market and geopolitical uncertainties, Clarksons Research reports a 54% year-on-year decline in global newbuild orders year-to-date. The Clarksons Newbuilding Price Index dipped 1% year-on-year.

The containership (1.9 million TEU in new orders), cruise, and ferry newbuilding markets remained active, while investment in gas carriers and tankers slowed. Newbuild deliveries stayed steady, with Chinese shipyards accounting for 48%, South Korea 31%, and Japan 13%. However, China’s share of new orders dropped from 70% in 2024 to 52%.

Secondhand vessel transactions fell 15% during the same period. Clarksons Research will release its Sale & Purchase Report and Vessel Asset Price Trends Training for valuation clients in the second half of the year.

Shipping’s Green Transition

Despite short-term challenges, the “green transition” remains a critical long-term trend with emerging opportunities. Clarksons Research notes that alternative-fueled vessels now make up 55% of the global orderbook, while energy-saving retrofits continue to rise.

The EU’s “Fit for 55” emissions package and IMO’s evolving mid-term measures are shaping regulatory progress. Ship recycling volumes remain historically low, potentially serving as a future “pressure valve” for the market.

{kind=link}