The figures presented in this report are unaudited. Figures in brackets, unless otherwise stated, refer to the same period a year earlier.

THIRD QUARTER HIGHLIGHTS

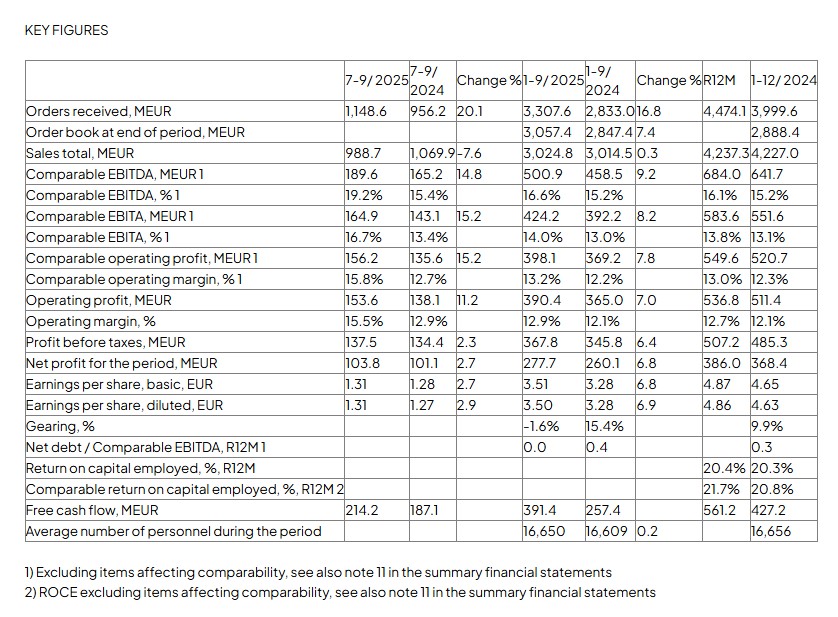

– Order intake EUR 1,148.6 million (956.2), +20.1 percent (+22.9 percent on a comparable currency basis), order intake increased in all Business Areas

– Industrial Service annual agreement base value EUR 334.6 million (328.9), +1.7 percent (+5.2 percent on a comparable currency basis)

– Order book EUR 3,057.4 million (2,847.4) at the end of September, + 7.4 percent (+9.2 percent on a comparable currency basis)

– Sales EUR 988.7 million (1,069.9), -7.6 percent (-5.5 percent on a comparable currency basis), sales decreased in Industrial Service and Port Solutions, but increased in Industrial Equipment

– Comparable EBITA margin 16.7 percent (13.4) and comparable EBITA EUR 164.9 million (143.1); the comparable EBITA margin increased to 22.7 percent (21.6) in Industrial Service, increased to 14.1 percent (9.8) in Industrial Equipment and increased to 11.8 percent (9.6) in Port Solutions.

– Operating profit EUR 153.6 million (138.1), 15.5 percent of sales (12.9)

– Earnings per share (diluted) EUR 1.31 (1.27)

– Free cash flow EUR 214.2 million (187.1)

JANUARY–SEPTEMBER 2025 HIGHLIGHTS

– Order intake EUR 3,307.6 million (2,833.0), +16.8 percent (+18.2 percent on a comparable currency basis)

– Sales EUR 3,024.8 million (3,014.5), +0.3 percent (+1.5 percent on a comparable currency basis)

– Comparable EBITA margin 14.0 percent (13.0) and comparable EBITA EUR 424.2 million (392.2); the comparable EBITA margin increased in Industrial Service and Port Solutions, but decreased in Industrial Equipment

– Operating profit EUR 390.4 million (365.0), 12.9 percent of sales (12.1), items affecting comparability totaled EUR 7.7 million (4.2), mainly comprising of restructuring costs

– Earnings per share (diluted) EUR 3.50 (3.28)

– Free cash flow EUR 391.4 million (257.4)

– Net debt EUR -31.3 million (266.9) and gearing -1.6 percent (15.4)

DEMAND OUTLOOK

Our demand environment within industrial customer segments has remained good and continues on a healthy level. However, the demand-related uncertainty and volatility due to the geopolitical and trade policy tensions remain.

Global container throughput continues on a high level, and long-term prospects related to global container handling remain good overall.

FINANCIAL GUIDANCE

Konecranes expects net sales to remain approximately on the same level in 2025 compared to 2024. Konecranes expects the full-year 2025 comparable EBITA margin to remain approximately on the same level or to improve from 2024.

CEO Marko Tulokas:

The third quarter of 2025 was excellent for Konecranes. Despite all the volatility and prevailing uncertainty in the operating environment, we delivered strong results once again. The market held up well throughout the quarter and our performance was robust across all our businesses. As a result, our comparable EBITA margin hit its highest level ever, order intake increased significantly and we had record-strong cash flow.

I am very pleased with our teams for delivering such a great quarter.

In the third quarter, our order intake increased by 22.9% in comparable currencies versus a year ago and was EUR 1.15 billion. Our sales amounted to nearly EUR 1.0 billion and decreased by 5.5% in comparable currencies. This development was mainly driven by a lower order book for the quarter in Business Area Port Solutions, where quarterly fluctuation is a normal feature of the business. Our comparable EBITA margin reached a new record-high level of 16.7% and was positively impacted by good execution and one-off items. At the end of the quarter, our order book totaled EUR 3.06 billion, reaching its highest level since the first quarter of 2024.

In Business Area Industrial Service, order intake increased by 8.7% and was positively impacted by a few large modernization projects. Sales amounted to EUR 383.1 million in the third quarter, remaining relatively stable compared to a year ago. Comparable EBITA margin increased and reached a level of 22.7%. The agreement base continued its positive trend and grew by 5.2% in comparable currencies. I am very pleased with this development since increasing the agreement base is fundamental for the service business’ growth, stability and strong margins.

In Business Area Industrial Equipment, performance was exceptionally strong in the third quarter. External order intake increased by 26.1% in comparable currencies versus a year ago. External sales also increased by 6.3% in comparable currencies and amounted to EUR 303.1 million. Comparable EBITA margin improved significantly to a level of 14.1% and reached its highest level ever. This major improvement compared to a year ago was mainly driven by volume but also one-off items and good execution. We have implemented structural improvements over the years and will continue to do so to strengthen the performance of this business.

In Business Area Port Solutions, performance remained solid in the third quarter. Order intake improved by 35.9% in comparable currencies versus a year ago. By nature, this business can fluctuate significantly from one quarter to another and in the third quarter we managed to lock in many projects. Sales decreased by 18.6% in comparable currencies to EUR 325.9 million in the third quarter. Despite lower volumes, comparable EBITA margin increased to 11.8% due to good execution and improved product mix. At the end of the quarter, Business Area Port Solutions’ order book totaled EUR 1.7 billion.

Tariffs continued to cause uncertainty in customer decision-making throughout the third quarter, especially in North America. Konecranes is well positioned in the global landscape, but we remain affected by the tariffs. We have been successful in managing their adverse impact through our own pricing actions and had a timing-related tailwind for the third quarter, but recently the situation has become more challenging. Moving forward, we expect the tariffs to cause some headwinds but not place us in a generally weaker position against our competition.

Our demand environment within industrial customer segments has remained good and continues on a healthy level. However, the demand-related uncertainty and volatility due to the geopolitical and trade policy tensions remain. Global container throughput continues on a high level, and long-term prospects related to global container handling remain good overall. Sales funnels in all Business Areas remain on a stable level.

We reiterate our financial guidance for this year.

We expect our net sales to remain approximately on the same level in 2025 compared to 2024. We also expect the full-year 2025 comparable EBITA margin to remain approximately on the same level or to improve from 2024.

At Konecranes we have a strong foundation to build on and drive long-term profitable growth. We have a global business model and strong presence in key regions. Our customer base is diverse and global, and our dual-channel market approach gives us comprehensive access to customers. As CEO I will foster these very important relationships also going forward. Our broad product and service lifecycle offering continues to give us an advantage when catering to our customers’ wide needs and creates stability against customer segment demand volatility.

I also aim to further leverage our lifecycle approach and technology leadership. We are not only providing equipment to our customers but also taking care of it during its lifetime. This is naturally business for us, but it’s also the only sustainable way to operate in today’s world. Also, reinforcing our technology leadership is crucial. Focusing even more on technology, innovation and development allows us to differentiate our leading offering versus competition and create even more value for our customers and shareholders.

We have a strong foundation and great teams in place to build on our success and drive for expansion and growth.

Source: Konecranes

{kind=link}