De-escalation eases risks, not fundamentals

The signing of a preliminary Memorandum of Understanding (MoU) between the US and Iran last week, alongside the extension of the ceasefire, has eased concerns over further disruptions to aluminium supply and key shipping routes in the Middle East. However, while the agreement lowers the risk of additional supply losses, it does not materially change our outlook for the aluminium market.

We continue to expect the global aluminium market to remain in deficit this year. Supply disruptions linked to the conflict have already removed an estimated 3 million tonnes of production from the market. As a result, we continue to forecast a global aluminium deficit of 1.8 million tonnes this year. While the geopolitical backdrop has improved, the supply losses underpinning this outlook remain in place.

The Middle East accounts for approximately 9% of global primary aluminium production and remains a key supplier to international markets. Earlier concerns centred not only on potential production losses but also on the risk of disruptions to shipping through the Strait of Hormuz, a critical route for both metals and energy flows. The ceasefire extension has eased these concerns and reduced the likelihood of a broader regional escalation.

Lost supply won’t return overnight

However, aluminium supply cannot be restored overnight. Smelters are designed to operate continuously, and restarting idled capacity can take months and require significant investment. This means that even if geopolitical conditions continue to improve, supply recovery is likely to be gradual. The ceasefire reduces the risk of further disruptions, but it does not immediately restore lost production.

China steps in, but can’t fill the gap

Higher Chinese exports have provided some relief to the market. Export volumes rose 15% year-on-year in April to 598kt and increased a further 16% year-on-year in May to 630kt, with the China Nonferrous Metals Industry Association (CNIA) suggesting that full-year aluminium product exports could reach a record high in 2026.

The increase in exports has been driven by a widening premium between international and Chinese aluminium prices following supply disruptions linked to the Middle East conflict. Higher prices outside China have encouraged producers to maximise exports, while weaker domestic demand and elevated inventories have also supported additional overseas shipments.

China has also increased alumina exports, with May shipments rising 36.4% year-on-year to 280kt. The increase in alumina availability has helped alleviate some concerns over raw material supply and provided additional support to global aluminium supply chains.

China’s ability to further increase supply also appears limited.

Annualised production is already running at around 46.7 million tonnes, above the government’s 45 million tonnes capacity cap. While higher export volumes have helped alleviate some of the tightness in global markets, there appears to be limited scope for a significant increase in Chinese output, leaving the global market dependent on a gradual recovery in disrupted supply elsewhere.

Additional supply growth from Indonesia is also unlikely to materially alter market balances in the near term. While new projects are expected to increase capacity, the estimated incremental supply additions of around 0.5-0.8 million tonnes this year, subject to downside risk from power and permitting constraints, are well below the estimated 3 million tonnes of production lost as a result of the Middle East conflict. As a result, the market is likely to remain in deficit despite rising output from Indonesia.

Aluminium remains supported

For prices, the ceasefire is likely to have a greater impact on risk sentiment than on fundamentals. During the height of the conflict, aluminium prices incorporated a geopolitical premium reflecting the possibility of further supply disruptions and shipping bottlenecks. With the ceasefire now extended and the US-Iran MoU providing a framework for further negotiations, part of this premium is likely to unwind.

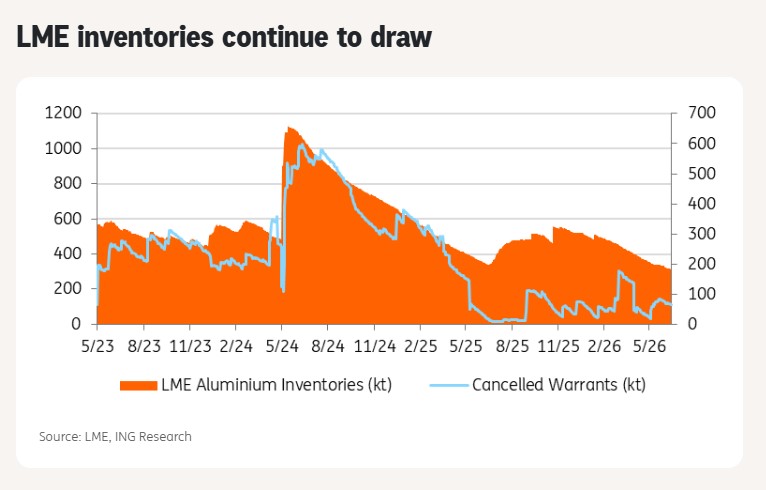

However, we believe downside risks for aluminium prices remain limited. The market continues to face a supply deficit of 1.8 million tonnes, while inventories continue to signal tight physical market conditions. LME aluminium stocks have fallen to around 314kt, down almost 40% from the start of the year despite stronger Chinese exports and the easing in geopolitical tensions.

The improvement in the geopolitical backdrop reduces the risk of further supply disruptions, but it does not immediately restore lost production. Chinese exports have not been sufficient to rebalance the market. As a result, we continue to see supportive fundamentals for aluminium despite the recent de-escalation. We maintain our aluminium price forecasts of $3,/t in 3Q and $3,/t in 4Q.

Source: ING

{kind=link}