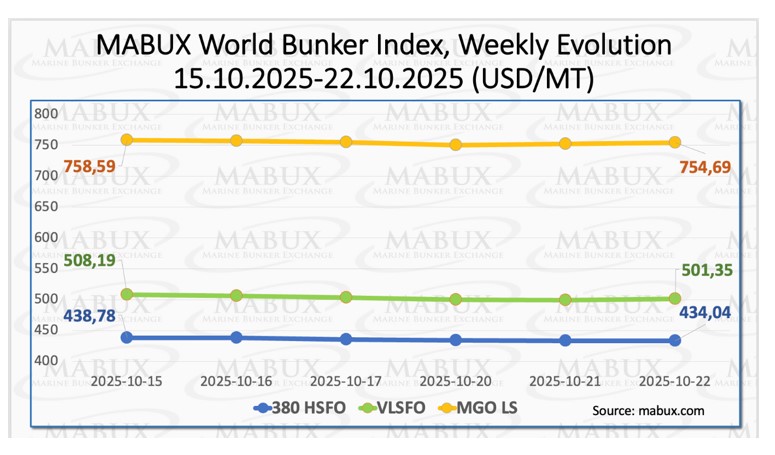

At the close of Week 43, global bunker indices tracked by MABUX continued their moderate downward trend. The 380 HSFO index declined by another USD 14.74, from USD /MT to USD /MT. The VLSFO index slipped by USD 6.84 (to USD /MT from USD /MT), moving closer to the USD /MT threshold. The MGO index also eased by USD 3.90, down from USD /MT to USD /MT. At the time of reporting, signs of an upward correction were emerging in the global bunker market.

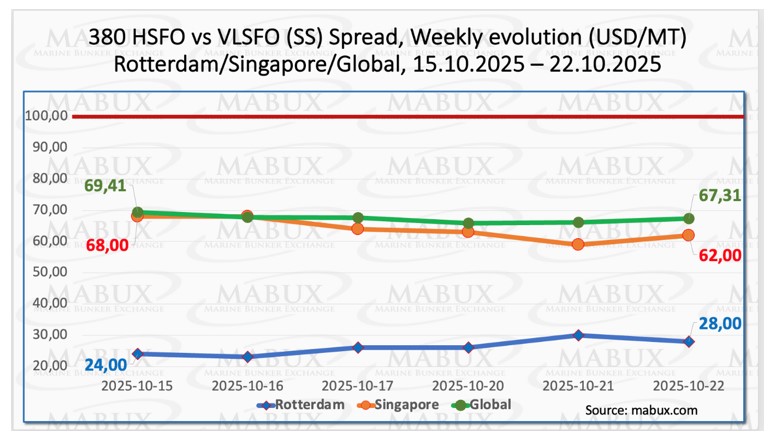

The MABUX Global Scrubber Spread (SS) — the price difference between 380 HSFO and VLSFO — continued to narrow, declining by USD 2.10 (from USD 69.41 last week to USD 67.31), moving further away from the USD 100.00 “breakeven” mark. The weekly average of the global SS index also decreased by USD 1.52. In Rotterdam, the SS Spread posted a moderate increase of USD 4.00 (up to USD 28.00 from USD 24.00 last week), though it remained near October 2024’s minimum levels. Conversely, the weekly average at the port declined by USD 4.33. In Singapore, the 380 HSFO–VLSFO differential fell by USD 6.00 (from USD 68.00 to USD 62.00), with the weekly average down by USD 6.83. Overall, the gradual narrowing of the SS Spread remains the prevailing trend in the global bunker market, supporting the higher profitability of conventional VLSFO compared to the HSFO + Scrubber combination. We expect this trend to persist into next week. Detailed figures are available in the “Differentials” section on .

According to the U.S. Energy Information Administration (EIA), North American liquefied natural gas (LNG) export capacity is projected to more than double by 2029 as new terminals come online in the United States, Canada, and Mexico. The agency forecasts capacity to increase from roughly 14 billion cubic feet per day (/d) in 2024 to over 29 /d by 2029. This surge will be driven primarily by the completion of seven major U.S. export terminals. Once fully operational, North America is expected to supply nearly 40% of global LNG volumes by the end of the decade, further strengthening the region’s role as a key player in the global gas market.

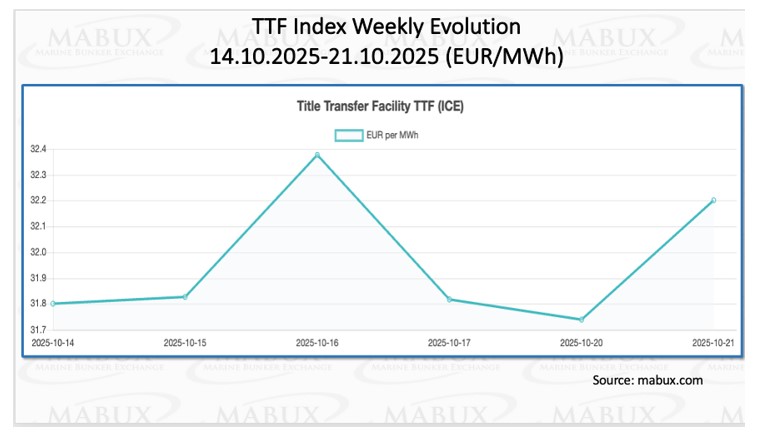

As of October 21, European regional gas storage facilities were 82.83% full, marking a decline of 0.26% from the previous week — the first negative movement since April this year. Current storage levels remain 11.50% higher than at the start of the year (71.33%). With the onset of lower temperatures, the rate of gas withdrawal has slightly exceeded the rate of injection, indicating the beginning of the seasonal drawdown phase. By the end of Week 43, the European gas benchmark TTF reversed its previous downward trend, rising by 0.399 /MWh to 32.200 /MWh from 31.801 /MWh a week earlier.

The price of LNG as a bunker fuel at the port of Sines (Portugal) posted a moderate gain this week, increasing by USD 3.00 to USD /MT from USD /MT a week earlier.

This uptick widened the price differential between LNG and conventional bunker fuel to USD 38 in favor of conventional fuel, a notable expansion from USD 10 the previous week. On the same day, MGO LS was assessed at USD /MT at the port of Sines. The growing price gap reflects a shift in short-term cost dynamics, potentially enhancing the competitiveness of conventional bunker fuels over LNG. More detailed data and analysis are available in the “LNG Bunkering” section of .

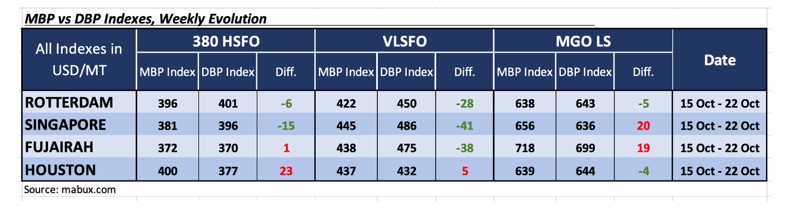

At the end of Week 43, the MABUX Market Differential Index (MDI) — which reflects the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP) — indicated the following bunker fuel price dynamics across the world’s major hubs: Rotterdam, Singapore, Fujairah, and Houston:

• 380 HSFO segment: Fujairah and Houston remained overvalued, with average weekly MDI values falling by 10 points in Fujairah but rising by 6 points in Houston. In contrast, Rotterdam and Singapore stayed undervalued, with the index declining by 8 and 2 points, respectively. MDI readings in Rotterdam and Fujairah approached the 100% correlation mark between MBP and DBP.

• VLSFO segment: Houston was the only overvalued port in this segment, with its average MDI rising by 5 points, maintaining a 100% correlation between MBP and DBP.

All other ports remained undervalued: the average weekly MDI fell by 6 points in Rotterdam, while it rose by 2 points in Singapore and 4 points in Fujairah.

• MGO LS segment: Singapore and Fujairah stayed in the overvalued zone, with MDI values increasing by 10 and 13 points, respectively. Rotterdam and Houston remained undervalued: Rotterdam’s MDI declined by 2 points, while Houston’s increased by 3 points. Both ports’ MDI levels are now close to the 100% correlation mark between MBP and DBP.

No significant shifts were observed in the overall balance of overvalued and undervalued ports last week. The SS Spread structure has reached a state of relative equilibrium, and we expect this balance to persist into the coming week.

More detailed information on the correlation between market prices and the MABUX digital benchmark is available in the Digital Bunker Prices section on .

According to the International Maritime Bureau (IMB), 116 incidents of maritime piracy and armed robbery were recorded in the first nine months of 2025 — a sharp increase from 79 incidents during the same period in 2024. This marks the highest number of reported cases for a nine-month period since 2021 and the highest level of incidents in the Singapore Strait since 1991. Of the total incidents, 102 vessels were boarded, nine experienced attempted attacks, four were hijacked, and one was fired upon. In 91% of cases, the assailants successfully boarded their targets, with the majority of attacks occurring at night. The IMB highlighted that the threat of violence against crew remains a critical concern, as weapons were used in 55% of reported cases. Notably, attackers were armed with firearms in 33% of incidents — the highest rate since 2017.

The impact on crew was significant: 43 seafarers were taken hostage, 16 were kidnapped, seven were threatened, three were beaten, and three sustained injuries. The Singapore Strait remained a hotspot, accounting for 73 incidents between January and September 2025. However, the IMB observed a marked decline in activity following the arrest of two criminal gangs by the Indonesian Maritime Police in July 2025, underscoring the effectiveness of targeted law enforcement operations.

Current market dynamics suggest that an upward trend is emerging in the global bunker market, supported by strengthening crude benchmarks and steady demand fundamentals. Consequently, bunker indices are expected to resume moderate growth in the forthcoming week.

Source: By Sergey Ivanov, Director, MABUX

{kind=link}