A shift in expectations around the long-term decline in oil demand in the recently released Inevitable Policy Response (IPR) Forecast Policy Scenario (FPS-2025) highlights diminishing climate-related vulnerabilities in certain sectors, Fitch Ratings says. It also illustrates the challenges of long-term forecasting, and such forecasts’ variability in the face of seemingly small changes in assumptions.

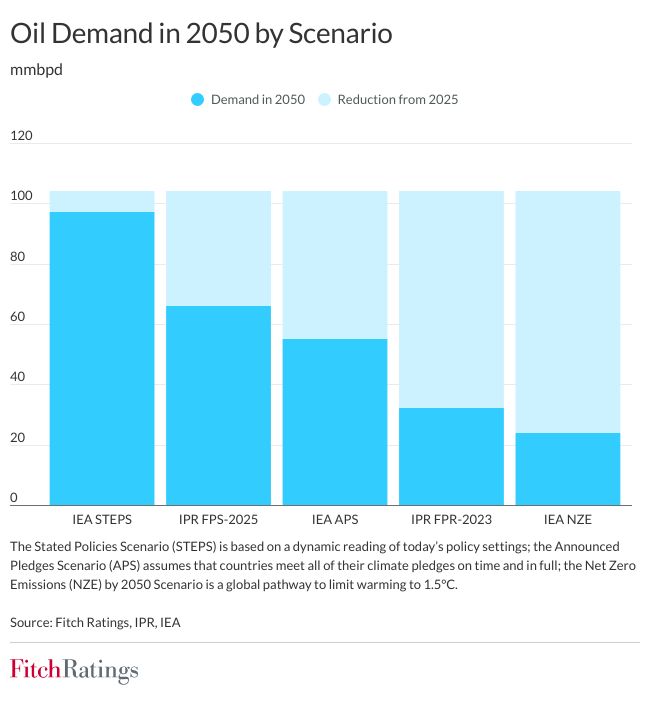

The relative reduction in oil demand by 2050 compared with FPS-2023 (updated in July 2024), which underpinned our previous Climate Vulnerability Signals (Climate.VS) analysis, has shifted from 62% to 33%, but with most of the changes occurring after 2035. The higher-than-previously-expected oil demand is driven by two factors: transportation (about 22 million barrels per day, or 22mmbpd, of additional demand versus FPS-2023) and non-energy use (over 10mmbpd of additional demand), primarily plastics.

Road transportation accounts for three quarters of transportation demand for oil. FPS-2025 incorporates slower electric vehicle (EV) take-up than the previous forecast and assumes new EV sales and EV penetration reaching 90% and 70%, respectively, in 2050 (compared with 100% and 94% in FPS-2023), resulting in higher demand for oil from both light- and heavy-duty vehicles.

The impact of this relatively small change in 2050 demand illustrates the high level of uncertainty involved in any long-term forecast. Further policy changes, as well as technological and economic developments, may significantly alter EV sales and other aspects of energy demand in the future. The variability in the range of oil demand outcomes is illustrated by a potential reduction in 2050 of only 7% under the International Energy Agency (IEA) Stated Policies Scenario, which compares to a reduction of more than three quarters based on the IEA Net Zero Emissions Scenario from 2025 levels of oil demand.

The uncertainty also illustrates the challenge sector participants face in determining appropriate investment in new projects, which is needed to maintain oil production. This uncertainty increases the risk of material over- or under-supply leading to increased price volatility, which in the long term could increase credit risk.

These factors lead Fitch to remain cautious regarding the potential risks posed by the energy transition to oil-related sectors, regardless of short-term policy choices in some parts of the world swinging towards oil producers, and resultant changes in scenarios.

Fitch is reviewing sector Climate.VS curves for its global corporate portfolio, where the IPR FPS is our central regulatory and policy risk scenario, and will publish an updated report in the coming weeks. We do not anticipate major changes to Climate.VS curves as a result of this review. Issuer Climate.VS curves are derived from sector Climate.VS curves, based on an analysis of revenue sources in the last full fiscal year. We do not expect any immediate rating implications as a result, given the very long-term time horizon of the changes in FPS-2025.

Source: Fitch Ratings

{kind=link}