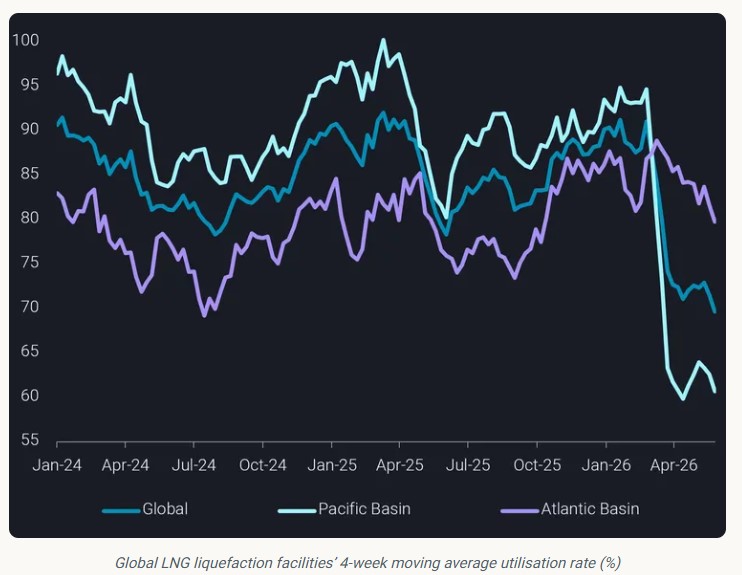

The Atlantic Basin has become the backbone of global LNG supply since March, owing to unprecedented disruption in the Middle East. Its market share increased from 44% in February to 55% in May 2026.

However, the overall utilisation rate of Atlantic Basin LNG export capacity has actually declined over the past couple of months. Its four-week moving average reached a high of 89% in early March, before falling to 80% in the week ending 31 May.

In truth, this does not mean there is material scope to unlock short-term production upside. If we exclude Russia’s sanctioned terminals (16 mtpa of nameplate capacity) and Egypt’s largely idle export facilities (12 mtpa), then Atlantic Basin utilisation averaged almost 100% in March and was still about 90% in May.

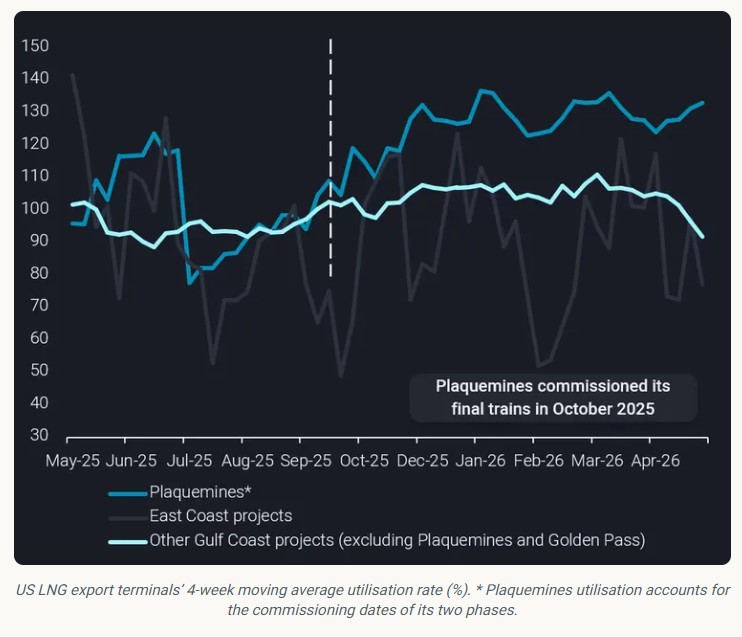

Most leading US liquefaction facilities have operated at above 100% of nameplate capacity for much of 2026. Outside the US, the largest Atlantic Basin terminals – Nigeria LNG and Russia’s Yamal LNG – have also outperformed recent years, respectively averaging about 90% and 120% utilisation.

Atlantic Basin LNG exports dropped from a record high of 18.5 mt in March to 17.7 mt in May. This is consistent with the market’s typical seasonal pattern, as it enters a shoulder season of lower demand when planned maintenance is common.

In the Northern Hemisphere summer, the global LNG utilisation rate is generally lower than in winter. Over the past three years, this metric has averaged 88% in Q1, compared with 81% between June and August. For the Atlantic Basin, average summer utilisation was 74% in 2023-25.

US projects stick to maintenance plans, despite market volatility

US LNG output has dipped in recent weeks as maintenance activity ramps up. In line with previous years, US Gulf Coast operators scheduled downtime from late spring, when demand is relatively lower.

The 16.5 mtpa Freeport facility entered planned maintenance in mid-May, with the work lasting several weeks. The 13.5 mtpa Cameron terminal also recently finished regular annual maintenance on one train, which took about 30 days, while Corpus Christi had a partial outage earlier in May. No prolonged downtime is expected in 2026 at Sabine Pass – the largest US liquefaction hub.

US LNG exporters previously indicated that they were reviewing maintenance schedules to potentially market more cargoes – to alleviate global supply concerns and benefit from elevated prices. However, operators mostly appear to be proceeding as planned with scheduled maintenance, ahead of the anticipated increase in Asia’s summer demand.

2026 hurricane forecast indicates low risk of US LNG disruption

The upcoming hurricane season, which lasts from June to November, is another critical factor that could impact US LNG exports.

This year, the National Weather Service is forecasting a “below-normal” Atlantic hurricane season, with 8-14 named storms. Of those, 3-6 are expected to become hurricanes, including 1-3 major hurricanes. By comparison, an average season has 14 named storms, of which seven are hurricanes, including three major hurricanes.

The 2025 hurricane season was forecasted to bring above-average activity. However, it ended with no hurricanes making landfall in the US. As a result, the impact on LNG operations was very limited. The most recent major hurricane-related disruption occurred in July 2024, when Hurricane Beryl caused US Gulf Coast power outages and loading delays. Storm-related damage forced Freeport LNG offline for two weeks.

If the 2026 hurricane season develops as anticipated, US LNG projects should experience relatively smooth operations.

Summer maintenance will partly offset supply gains from Atlantic Basin’s newest terminals

In the coming months, Atlantic Basin net supply growth will be delicately poised, as maintenance outages could balance out incremental volumes from the latest start-ups. In the US, Golden Pass’s 6 mtpa Train 1 is still in its early commissioning ramp-up. By end-May, it had shipped only two cargoes in the six weeks since entering service in April.

Nor will downtime be limited to the US. In Trinidad and Tobago, Atlantic LNG’s 5.2 mtpa Train 4 went offline in late May for over 50 days of scheduled maintenance, which will extend into July. In addition, the 5.2 mtpa Angola LNG facility will undergo maintenance in July-August.

As the market transitions into the summer demand season, the global LNG balance will stay heavily reliant on Atlantic Basin supply.

The timing of a full reopening of the Strait of Hormuz remains unclear. However, even if this surprises to the upside, Qatar’s output will still take several months to recover. Given this, the outlook in the US for both low hurricane-related disruption and relatively light maintenance should provide some much-needed relief to a tight supply picture.

Source: Vortexa

{kind=link}