Data reported throughout April 2026, based on Alphaliner proprietary datasets and AIS-derived vessel tracking, highlighted how geopolitical disruption in the Middle East continued to reshape container shipping dynamics.

Across the month, vessel movements through the Strait of Hormuz remained severely constrained, liner participation declined further, and operational risks escalated following direct attacks on container ships. At the same time, structural trends such as fleet expansion and strong capacity utilization persisted, keeping overall market conditions tight despite widespread disruption.

Hormuz Transits Remained Severely Restricted Despite Ceasefire Developments

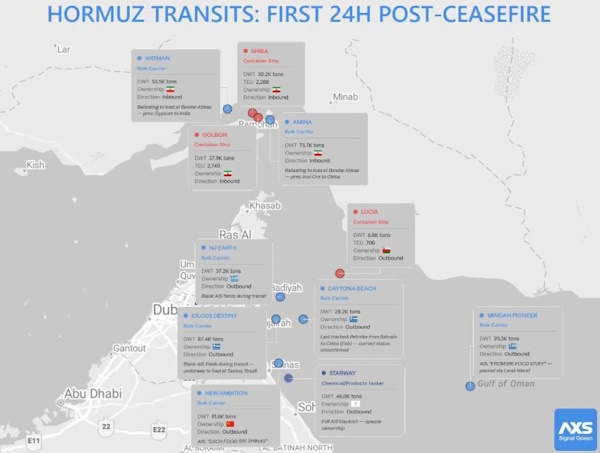

Data reported in April showed that container ship activity across the Strait of Hormuz remained largely unchanged following the announcement of a US–Iran ceasefire.

Within 24 hours of the announcement, only three container ships transited the Strait, including two Iranian-owned vessels inbound and one small feeder outbound. While this was above the March average of fewer than one vessel per day, it remained extremely limited by historical standards.

Crucially, these movements did not signal any meaningful return of international liner operations. Since the onset of the crisis, only a handful of large non-Iranian vessels completed isolated transits, including ships operated by Maersk, COSCO, and CMA CGM.

Overall, container traffic through Hormuz remained sporadic and highly selective, with activity largely concentrated among Iranian-linked and regional feeder operations.

Direct Attacks on Container Ships Marked a Clear Escalation

Developments during April also showed a clear escalation in operational risk for container shipping in the region.

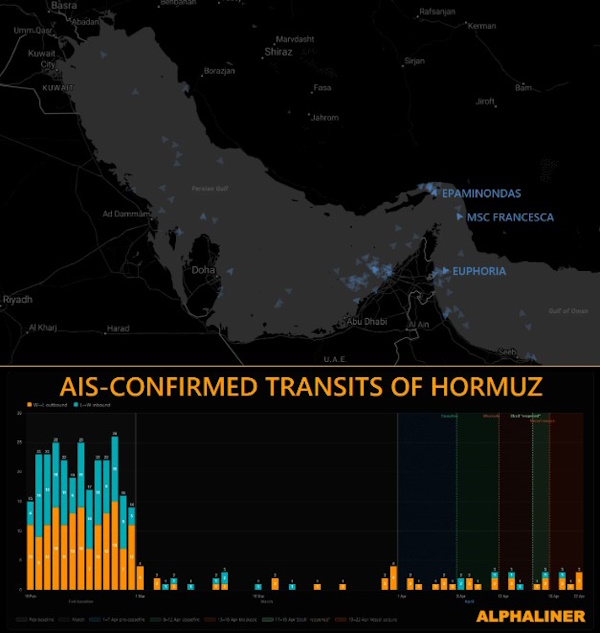

Three non-Iranian container ships attempting to transit the Strait came under direct attack, with two subsequently seized. Among them was the MSC FRANCESCA, operated by MSC, alongside the EPAMINONDAS and EUPHORIA.

These incidents reinforced a broader pattern observed throughout the month.

AIS-derived data recorded 54 container ship crossings over a 53-day period since early March, with roughly half linked to Iranian ownership or domestic routes.

The remaining crossings were dominated by smaller feeder and regional vessels, with only a limited number of deepsea liner ships attempting passage.

Notable exceptions included isolated transits by Maersk, COSCO SHIPPING, CMA CGM, and a late reappearance of a Hapag-Lloyd-linked vessel after an extended AIS blackout.

Overall, April data confirmed that international liner participation had become both sporadic and increasingly exposed to risk, while parallel regional activity continued under more opaque ownership structures.

Global Container Fleet Continued to Reach New Capacity Milestones

Despite regional disruption, structural fleet growth remained a defining trend throughout April.

Global container ship capacity surpassed 34 million TEU, with approximately 33.6 million TEU accounted for by the fully cellular fleet. This marked a new milestone for the industry.

At the carrier level, MSC extended its lead further, with fleet capacity exceeding 7.3 million TEU and representing around 21.6 percent of the global fleet.

Capacity deployment also continued to expand on key trade lanes. Weekly volumes on the Far East–Europe corridor exceeded 540,000 TEU, setting another record and continuing the upward trend observed earlier in the year.

These developments highlighted a key contrast:

fleet expansion and capacity growth continued largely unaffected, even as major trade corridors remained disrupted.

Market Remained Fully Employed as Disruption Absorbed Capacity

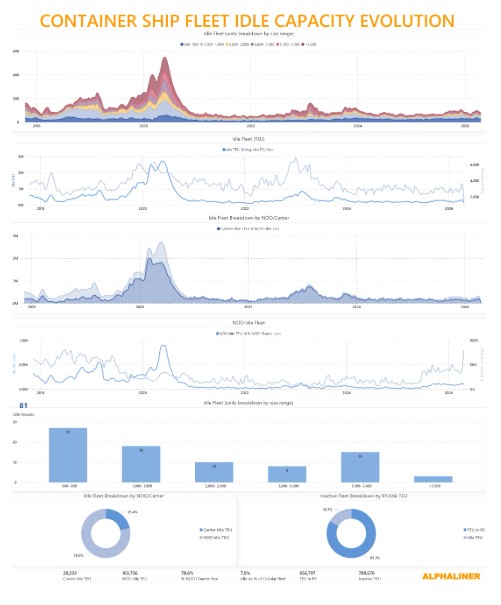

Fleet utilization data reported throughout April showed that the container shipping market remained tightly balanced.

Commercial idling fluctuated around 0.7 percent of global capacity, briefly approaching 1 percent before declining again. At these levels, the market remained effectively in full employment, with no signs of structural oversupply.

However, this headline figure understated the true supply situation.

At least 58 container ships, representing around 310,000 TEU, were reported as diverted or sheltered due to the Gulf conflict.

These vessels were not counted as commercially idle but were effectively removed from active supply.

This “forced inactivity” continued to tighten the market, as vessels were absorbed by:

• Service rerouting and network adjustments

• Longer voyage distances

• Port congestion at alternative hubs

Capacity tied up in shipyards also declined modestly during the month, with the combined idle and in-yard fleet accounting for just 2.7 percent of total capacity.

Key Takeaways

• Container ship transits through Hormuz remained extremely limited throughout April

• Direct attacks on vessels marked a clear escalation in operational risk

• Global fleet capacity exceeded 34 MTEU, with MSC surpassing 7.3 MTEU

• Record capacity deployment continued on the Far East–Europe trade

• Vessel idling remained low, partly due to capacity being tied up and unavailable

Stay Ahead with the Latest Insights

The container ship data trends reported in April 2026 reflected a market shaped by the interaction of geopolitical disruption and ongoing structural expansion.

While fleet growth and strong utilization continued to support overall market balance, the situation in the Middle East introduced significant operational constraints that reduced effective capacity and altered vessel deployment patterns.

As long as access through the Strait of Hormuz remained restricted and risks persisted, global shipping networks continued to adapt through rerouting, selective participation, and reliance on alternative corridors.

AXSInsights is one of many solutions available in the Alphaliner platform providing real-time data visibility and remains essential for understanding the container shipping market.

Source: AXSMarine

{kind=link}