In the first half of this year, the newbuilding market for container ships remained robust, with global orderbooks hitting a historic high. During this boom cycle, Chinese shipbuilders have strengthened their position, securing a 74% market share of the orderbook. This not only solidifies their dominance in the global shipbuilding market but also reinforces their influence in high-end vessel segments.

Clarksons noted in a recent report that while global newbuilding orders in 2025 declined compared to the record-breaking 2024, container ship orders continued to grow strongly. Since the beginning of this year, new container ship orders have reached 201 vessels totaling approximately 1.92 million TEU. Although growth has slowed compared to 2024’s peak of 4.6 million TEU, the figure remains twice the average of the past decade.

In terms of CGT, container ship orders in the first half of the year reached 8.7 million CGT, accounting for about half of global new orders. Chinese shipbuilders maintained their leading position in the container ship market, securing 134 orders totaling 1.17 million TEU, representing a 61% market share.

The sustained surge in orders has pushed the global container ship orderbook to 921 vessels totaling 9.42 million TEU—a 50% increase year-on-year and 20% higher than the recent peak of 7.79 million TEU in March 2023. The current orderbook represents 30% of the existing fleet capacity, still substantial though far below the 2008 historical high of 60%.

Source: Clarksons

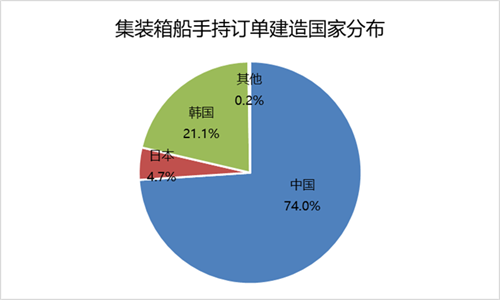

The vast majority of container ship orders are held by Chinese shipbuilders. According to Clarksons, Chinese yards currently hold 701 orders for 6.94 million TEU, capturing a 74% market share by TEU. South Korean shipbuilders follow with 157 orders for 1.98 million TEU (21.1% share), while Japanese yards hold 44 orders for 440,000 TEU (4.7% share).

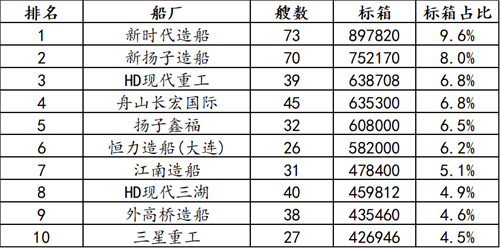

Top 10 Shipyards by Container Ship Orderbook

Among the top 10 global shipyards by container ship orderbook, seven are Chinese. These include the top two—New Times Shipbuilding (73 vessels, ~900,000 TEU) and New Yangzi Shipbuilding (70 vessels, ~750,000 TEU)—as well as Changhong International (Zhoushan) (45 vessels, ~640,000 TEU), Yangzijiang Xinfu (32 vessels, ~610,000 TEU), Hengli Heavy Industry (Dalian) (26 vessels, ~580,000 TEU), and Jiangnan Shipyard (31 vessels, ~480,000 TEU), ranked fourth to seventh, respectively. Additionally, Waigaoqiao Shipbuilding ranks ninth with 38 vessels (~440,000 TEU).

Meanwhile, only three South Korean shipyards made the top 10: HD Hyundai Heavy Industries (39 vessels, ~640,000 TEU) in third place, HD Hyundai Samho (40 vessels, ~460,000 TEU) in eighth, and Samsung Heavy Industries (27 vessels, ~430,000 TEU) in tenth.

In contrast, in June last year, South Korean shipyards led the rankings, with Samsung Heavy Industries and HD Hyundai Heavy Industries taking the top two spots. Yangzijiang Xinfu ranked third, followed by HD Hyundai Samho and Hanwha Ocean in fourth and fifth. New Yangzi Shipbuilding ranked sixth, Japan’s Imabari Shipbuilding (Hiroshima) seventh, while Jiangnan Shipyard, Waigaoqiao Shipbuilding, and Changhong International (Zhoushan) placed eighth to tenth. At the time, New Times Shipbuilding ranked only 12th with 22 vessels in its orderbook.

It is reported that New Times Shipbuilding secured dozens of container ship orders during the record-breaking 2021-2022 ordering wave. However, as the container ship newbuilding boom waned in 2023, the shipyard shifted its focus back to tankers. In the second half of last year, New Times Shipbuilding re-entered the container ship market, securing 62 orders—all for LNG dual-fuel vessels—within six months.

Similarly, Hengli Heavy Industry (Dalian), currently ranked sixth in the orderbook, entered the container ship market for the first time in September last year with an order for 10 dual-fuel LNG-powered 21,000 TEU vessels from MSC, the world’s largest container line. Within a year, MSC added another 10 24,000 TEU and six 22,000 TEU dual-fuel container ships to its orderbook.

Likewise, most of Changhong International’s orders come from MSC. Of its 45 container ship orders, 35 were placed by MSC, including nine 11,500 TEU, ten 10,300 TEU, twelve 19,000 TEU, and four 21,700 TEU vessels.

Clarksons highlighted multiple factors driving container ship orders. Following recent trends, liner companies remain the primary investors, accounting for 80% of this year’s new orders—similar to 2024—and now directly own about 63% of the global fleet. Fleet renewal for fuel transition is a key driver, with 73% of new orders being dual-fuel vessels (59% LNG-powered, 14% methanol-powered).

Since early 2024, strong earnings from high freight rates due to Red Sea diversions, recent alliance restructuring, and competitive repositioning have enabled liner companies to continue ordering. Tight shipyard berth availability has also prompted owners to secure slots early. Of this year’s orders, 74% are scheduled for delivery in 2024 or later.

Clarksons noted that the growing orderbook will significantly reshape the market in coming years, with deliveries scheduled through 2029-2030. A new delivery peak is expected in 2027-2028, with annual deliveries exceeding 2.5 million TEU. Even accounting for potential delays, future deliveries could approach 2024’s record of 3 million TEU.

Clarksons emphasized that last year’s record deliveries expanded the global container fleet by 10%, but this supply growth was largely absorbed by an 11% demand increase from Red Sea diversions. However, capacity pressures may emerge or intensify in the coming years, making the management of this new delivery wave a critical challenge for the industry.

{kind=link}