Weekly Special Focus

Increasing U.S. pressure on Russian oil buyers is driving China and India to cut imports and diversify their supply sources.

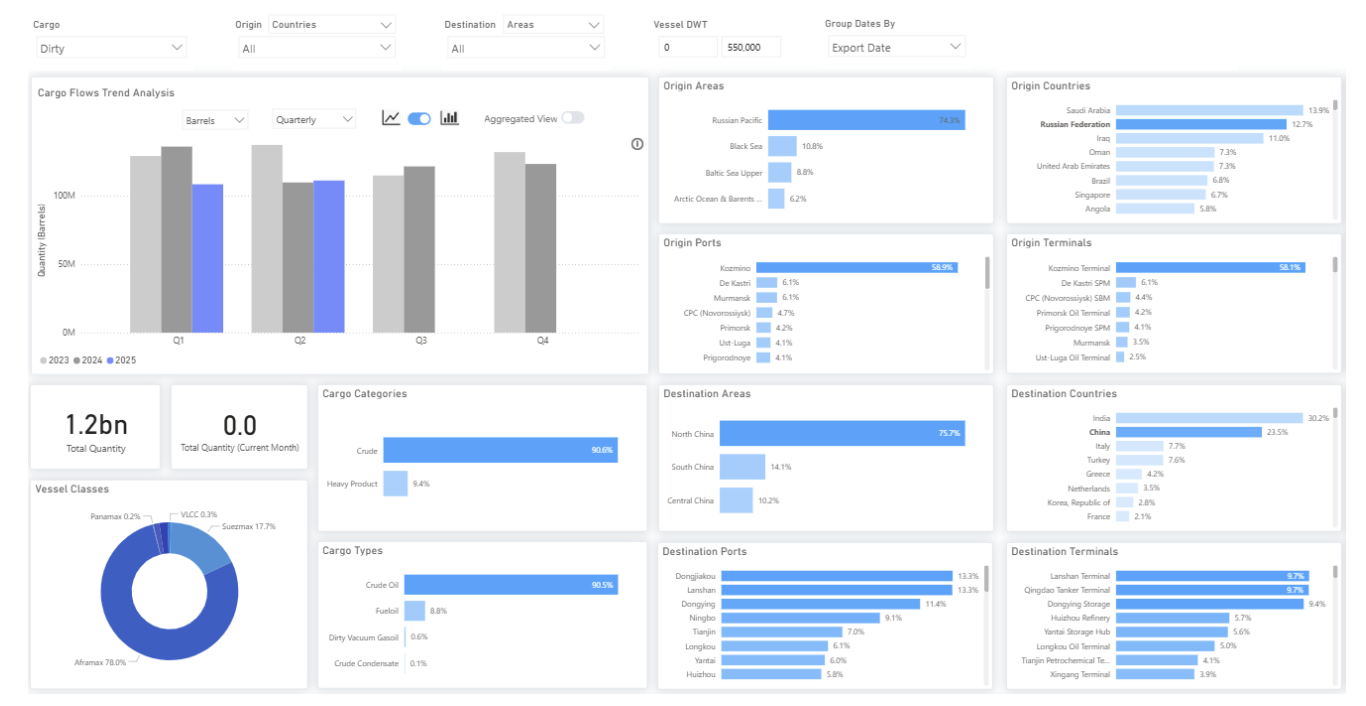

Russian Dirty Oil Exports to China

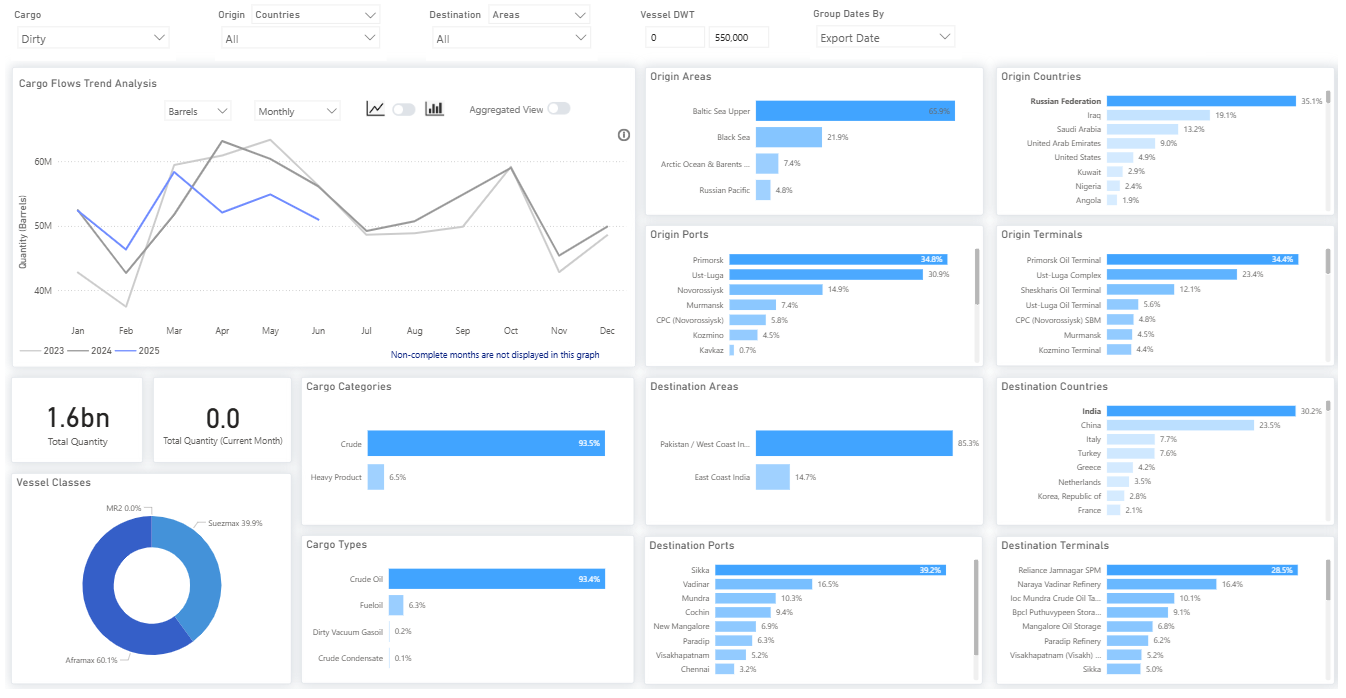

Indian import volumes show a milder decline: quarterly figures remained nearly unchanged compared to Q1 2025 but dropped roughly 12% year-over-year. However, monthly data indicates a steady decrease since March, with June shipments falling by over 10 million barrels.

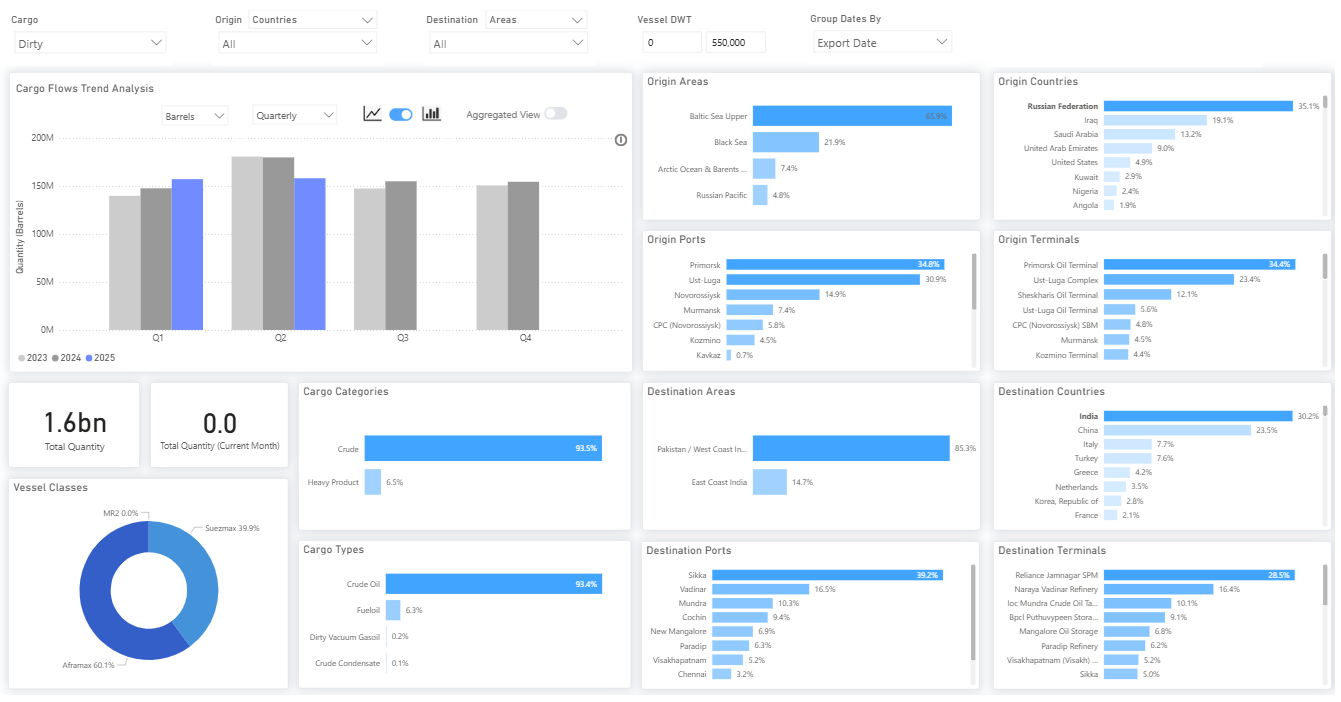

Russian Dirty Oil Exports to India (Quarterly)

Russian Dirty Oil Exports to India (Monthly)

It’s crucial to note that Russian crude oil remains legally available in Asia. While the EU and UK have unilaterally lowered the G7 price cap to $/bbl, the U.S. has resisted supporting this change, limiting the global enforceability of the revised cap—especially given oil’s dollar-denominated trade and U.S.-controlled payment systems. Neither the U.S. nor the EU has prohibited crude exports to India or China, indicating that recent import reductions by these nations are likely motivated by market pricing rather than sanctions evasion.

As of July 18, 2025, Brent crude traded near $70/bbl, while Urals crude was priced around $58/bbl FOB, maintaining a discount of roughly $12/bbl. Though still significant, this spread has widened compared to previous months when reduced Asian spot purchases temporarily narrowed the gap.

Several commercial and logistical factors are diminishing the appeal of Russian spot crude. A growing share of Russian exports is now sold under term contracts, reducing spot availability. Simultaneously, higher domestic refinery runs in Russia are tightening export supply. These dynamics have gradually pushed Urals prices higher, eroding the arbitrage advantage for Asian refiners. Consequently, price-sensitive buyers in India and China are likely scaling back opportunistic purchases rather than implementing a coordinated strategic shift.

This interpretation is further supported by tanker activity. In June, Greek-owned tankers notably resumed Russia-linked trades, suggesting improved logistical and compliance confidence, with sanctions risks being carefully managed rather than entirely avoided.

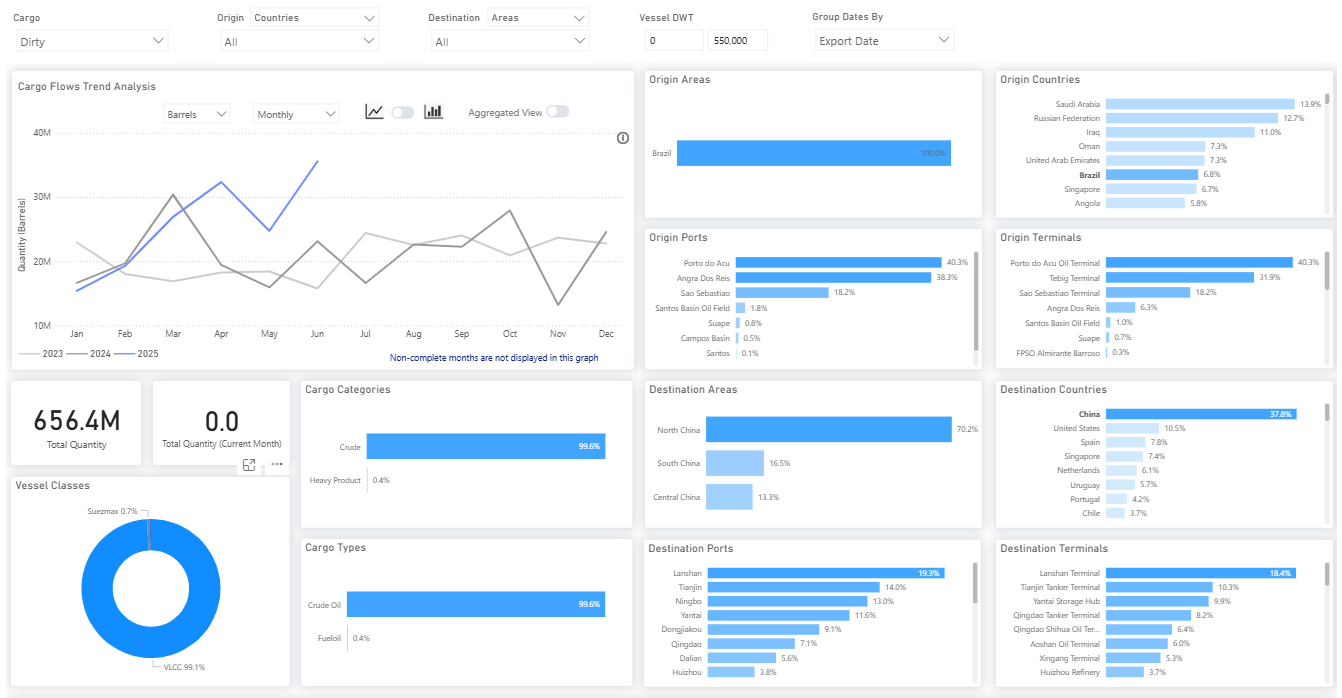

Meanwhile, Brazilian crude exports to China surged to over 30 million barrels in June, nearly double the 16 million barrels recorded in June 2023. These shipments primarily consist of heavy-sweet grades, offering similar yields to Russian Urals and aligning with China’s diversification strategy. While the increase doesn’t yet signal a significant rise in tonne-miles, it reflects a more diversified supply landscape for China, driven mainly by seasonal demand and relative value.

Brazilian Dirty Oil Exports to China (Monthly)

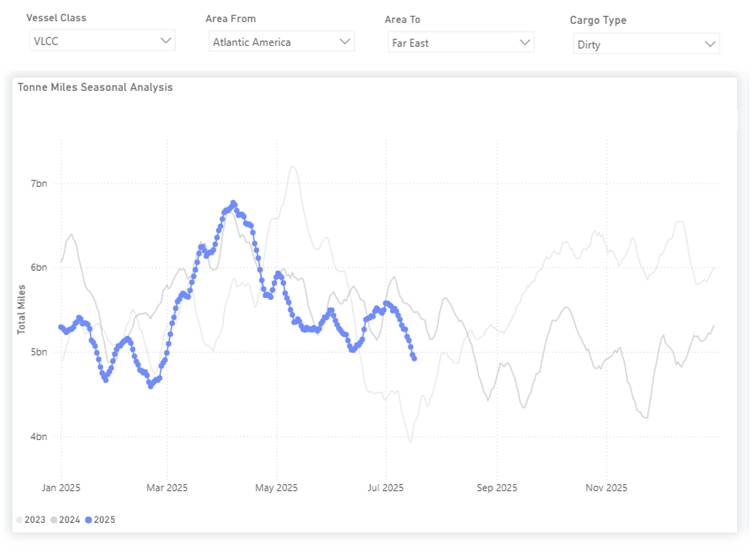

VLCC Tonne-Miles Seasonal Analysis: Brazil–China

This emerging trend of longer-haul Atlantic Basin crude flows into Asia may force Europe to rely more heavily on Middle Eastern and U.S. supplies. Such rebalancing could affect U.S. refiners—particularly those optimized for light sweet grades—by altering feedstock availability, margins, and output strategies. Concurrently, these shifts may bolster transatlantic clean product flows from the U.S. Gulf Coast to Europe, especially for ULSD and, to a lesser extent, naphtha. This could boost demand for clean product tankers, particularly MRs and LR1s, while gasoline exports are expected to remain concentrated in the Europe-to-U.S. Atlantic Coast trade.

Source: Signal Ocean

{kind=link}